Looking back at the housing market in 2023 and what we can expect in 2024, Robert Gardner, Nationwide’s Chief Economist, comments:

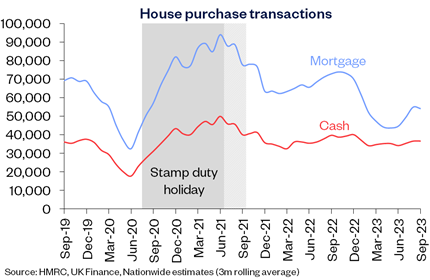

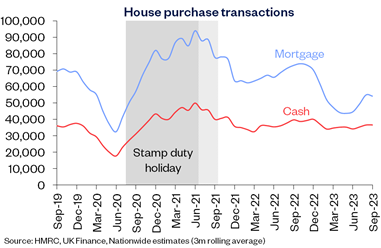

“Housing market activity was weak throughout 2023. The total number of transactions has been running at c15% below pre-pandemic levels over the past six months, with those involving a mortgage down even more (c25%), reflecting the impact of higher borrowing costs. On the flip side, cash transactions have been running above pre-Covid levels.

“This subdued picture was also reflected in house prices, which in November were 2% lower than the same period in 2022, and 4.3% below the all-time high recorded in late summer 2022.

Affordability pressures exerting a strong drag

“Even though house prices are modestly lower and incomes have been rising strongly, at least in cash terms, this hasn’t been enough to offset the impact of higher mortgage rates, which are still more than three times the record lows prevailing in 2021 in the wake of the pandemic.

“As a result, housing affordability is still stretched. A borrower earning the average UK income and buying a typical first-time buyer property with a 20% deposit would have a monthly mortgage payment equivalent to 38% of take home pay – well above the long run average of 30%.

“At the same time, deposit requirements remain prohibitively high for many of those wanting to buy – a 20% deposit on a typical first-time buyer home equates to over 105% of average annual gross income – down from the all-time high of 116% recorded in 2022, but still close to the pre-financial crisis level of 108%.

Where next in 2024?

“There have been some encouraging signs for potential buyers recently with mortgage rates edging down. Investors have become more optimistic that the Bank of England has already raised rates far enough to return inflation to target and will reduce rates in the years ahead. This shift in view is important, as it has brought down longer term interest rates which underpin fixed mortgage rate pricing.

“Nevertheless, a rapid rebound in activity or house prices in 2024 appears unlikely. While cost-of-living pressures are easing, with the rate of inflation now running below the rate of average wage growth, consumer confidence remains weak, and surveyors continue to report subdued levels of new buyer enquiries. Moreover, while markets are projecting that the next Bank Rate move will be down, there are still upward risks to interest rates. Inflation is declining, but measures of domestic price pressures remain far too high.

“It appears likely that a combination of solid income growth, together with modestly lower house prices and mortgage rates, will gradually improve affordability over time, with housing market activity remaining fairly subdued in the interim. If the economy remains sluggish and mortgage rates moderate only gradually, as we expect, house prices are likely to record another small decline (low single digits) or remain broadly flat over the course of 2024.”

-ends-