|

Headlines |

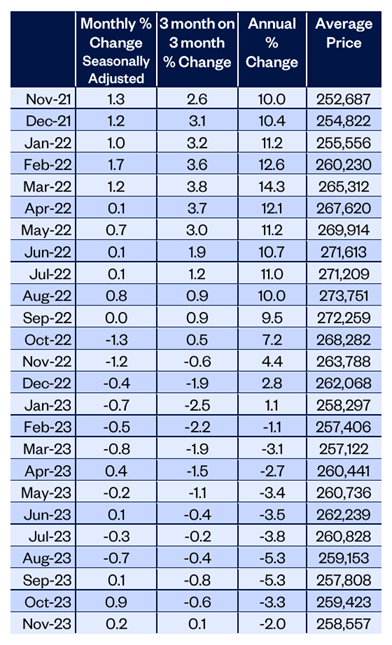

Nov-23 |

Oct-23 |

|

Monthly Index* |

518.0 |

516.8 |

|

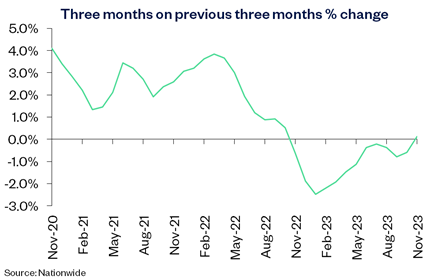

Monthly Change* |

0.2% |

0.9% |

|

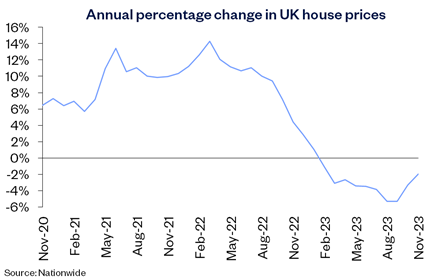

Annual Change |

-2.0% |

-3.3% |

|

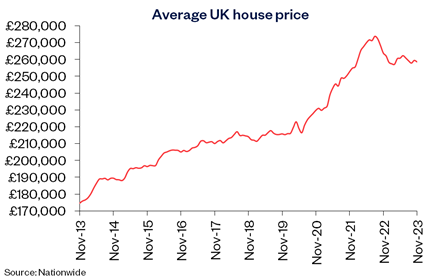

Average Price (not seasonally adjusted) |

£258,557 |

£259,423 |

* Seasonally adjusted figure (note that monthly % changes are revised when seasonal adjustment factors are re-estimated)

Commenting on the figures, Robert Gardner, Nationwide's Chief Economist, said:

“UK house prices rose by 0.2% in November, after taking account of seasonal effects. This was the third successive monthly increase and resulted in an improvement in the annual rate of house price growth from -3.3% in October, to -2.0%. While this remains weak, it is the strongest outturn for nine months.

Shift in interest rate expectations eases affordability pressures

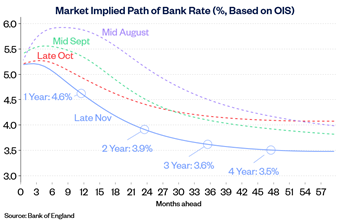

“There has been a significant change in market expectations for the future path of Bank Rate in recent months which, if sustained, could provide much needed support for housing market activity.

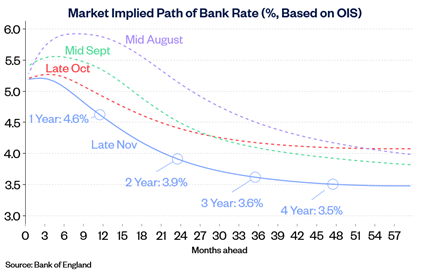

“In mid-August, investors had expected the Bank of England to raise rates to a peak of around 6% and lower them only modestly (to c.4%) over the next five years. By the end of November, this had shifted to a view that rates have now peaked (at 5.25%) and that they will be lowered to around 3.5% in the years ahead.

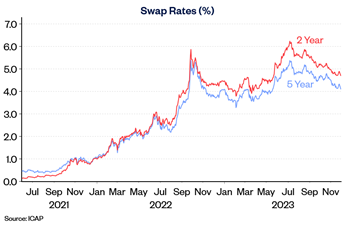

“These shifts are important as they have led to a decline in the longer-term interest rates (swap rates) that underpin fixed rate mortgage pricing, as shown below. If sustained, this will help to ease the affordability pressures that have been stifling housing market activity in recent quarters, where the number of mortgage approvals for house purchases has been running at c.30% below pre-pandemic levels.

“While mortgage rates are unlikely to return to the lows prevailing in the aftermath of the pandemic, modestly lower borrowing costs, together with solid rates of income growth and weak/negative house price growth, should help underpin a modest rise in activity in the quarters ahead.

“Nevertheless, a rapid rebound still appears unlikely. Cost-of-living pressures are easing, with the rate of inflation now running below the rate of average wage growth, but consumer confidence remains weak, and surveyors continue to report subdued levels of new buyer enquiries.

“Moreover, while markets are projecting that the next Bank Rate move will be down, there are still upward risks to interest rates. Inflation is declining, but measures of domestic price pressures remain far too high.

“Policymakers have cautioned that it is too early to be talking about interest rate cuts. Indeed, three of the nine members of the Bank of England’s Monetary Policy Committee voted to increase Bank Rate at its meeting in early November, though the remaining six preferred to hold at 5.25% for the time being.”

-ends-