|

Headlines |

Jul-22 |

Jun-22 |

|

Monthly Index* |

538.0 |

537.5 |

|

Monthly Change* |

0.1% |

0.2% |

|

Annual Change |

11.0% |

10.7% |

|

Average Price (not seasonally adjusted) |

£271,209 |

£271,613 |

* Seasonally adjusted figure (note that monthly % changes are revised when seasonal adjustment factors are re-estimated)

Commenting on the figures, Robert Gardner, Nationwide's Chief Economist, said:

“July saw a modest increase in the rate of annual house price growth to 11.0%, from 10.7% in June. Prices rose by 0.1% month-on-month, after taking account of seasonal effects – the twelfth successive monthly increase, which kept annual price growth in double digits for the ninth month in a row.

“The housing market has retained a surprising degree of momentum given the mounting pressures on household budgets from high inflation, which has already driven consumer confidence to all-time lows. While there are tentative signs of a slowdown in activity, with a dip in the number of mortgage approvals for house purchases in June, this has yet to feed through to price growth.

“Demand continues to be supported by strong labour market conditions, where the unemployment rate remains near 50-year lows and with the number of job vacancies close to record highs. At the same time, the limited stock of homes on the market has helped keep upward pressure on house prices.

“We continue to expect the market to slow as pressure on household budgets intensifies in the coming quarters, with inflation set to reach double digits towards the end of the year. Moreover, the Bank of England is widely expected to raise interest rates further, which will also exert a cooling impact on the market if this feeds through to mortgage rates.

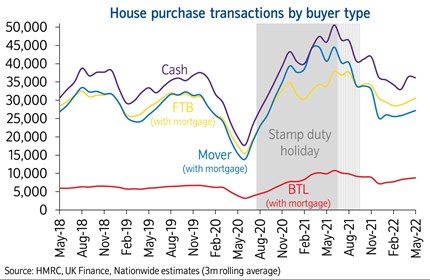

Strength in transactions across buyer types

“Total housing market transactions in the three months to May were c.20% below the elevated levels resulting from the stamp duty holiday, but 5% above pre-pandemic levels.

“Home mover transactions (with a mortgage) have slowed more than other sectors. This probably reflects that the stamp duty holiday had more of an impact encouraging home movers to bring forward purchases, particularly for higher value properties, with no Stamp Duty Land Tax (SDLT) payable up to £500,000 for completions by the end of June 2021. Behavioural shifts due to the pandemic are also likely to have provided more of a boost to home mover activity, where such drivers have now faded.

“First time buyer mortgage completions have remained resilient, and are now c.5% above pre-pandemic levels, despite growing affordability pressures. Indeed, house price growth has continued to outpace earnings by a wide margin, increasing the deposit hurdle, and, together with higher interest rates, has pushed up mortgage repayments relative to incomes.

“The number of cash transactions has remained elevated, though its share of activity has remained broadly stable at c.35%. This is partly a reflection of an ageing population (where more people own their homes outright). However, properties purchased for investment, such as a holiday home or buy to let, is also an important element of the cash market.

“Buy to let purchases involving a mortgage also remain higher than pre-pandemic levels. Sentiment is likely buoyed by the fact that rental demand remains strong, with upward pressure on rents, which may be encouraging landlords to enter the market, particularly if they view property as a hedge against inflation.”

-ends-