|

Headlines |

Aug-22 |

Jul-22 |

|

Monthly Index* |

543.3 |

539.1 |

|

Monthly Change* |

0.8% |

0.2% |

|

Annual Change |

10.0% |

11.0% |

|

Average Price (not seasonally adjusted) |

£273,751 |

£271,209 |

* Seasonally adjusted figure (note that monthly % changes are revised when seasonal adjustment factors are re-estimated)

Commenting on the figures, Robert Gardner, Nationwide's Chief Economist, said:

“While annual house price growth softened in August, it remained in double digits for the tenth month in a row – at 10.0%. Prices rose by 0.8% month-on-month, after taking account of seasonal effects – the thirteenth successive monthly increase. Indeed, in the past two years, the average house price has increased by almost £50,000.

“There are signs that the housing market is losing some momentum, with surveyors reporting fewer new buyer enquiries in recent months and the number of mortgage approvals for house purchases falling below pre-pandemic levels. However, the slowdown to date has been modest, and combined with a shortage of stock on the market, has meant that price growth has remained firm.

“We expect the market to slow further as pressure on household budgets intensifies in the coming quarters, with inflation set remain in double digits into next year. Moreover, the Bank of England is widely expected to continue raising interest rates, which will also exert a cooling impact on the market if this feeds through to mortgage rates, which have already increased noticeably in recent months.

Energy price cap increase will have greatest impact for least energy efficient properties

“Ofgem recently announced an 80% increase in the energy price cap, effective from 1 October, which reflects the soaring cost of energy in wholesale markets. It is important to note that the cap is on the unit price charged to consumers, rather than a maximum bill a household can be charged. So, while a typical household is set to pay £3,545 a year, for some costs will be even higher.

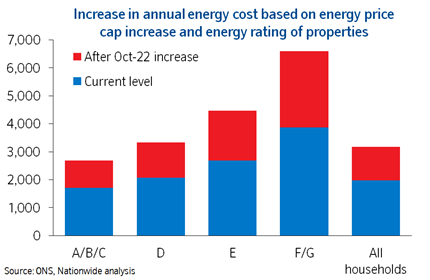

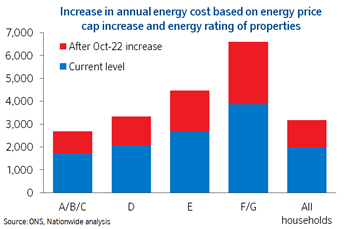

“We’ve looked at the impact of rising energy costs on average bills for properties with different energy efficiency ratings (as reported on energy performance certificates). Currently (based on the April 2022 price cap), the most energy efficient properties (those rated A-C) pay £1,700 per year, whilst the least efficient (those rated F-G) typically see bills over twice as high at c.£3,900 p.a.

“As things stand, from October, average bills for D-rated properties (the most common type) are set to rise by just over £1,250 a year, even after taking account of the government’s £400 discount. Those in properties rated A-C will see average bills increase by nearly £1,000 a year (or over £80 per month). E-rated properties will see an increase of over £1,700 per year (c. £150 per month), whilst those in the least energy efficient properties (F/G) face a staggering £2,700 rise (£225 per month). While only a small proportion of the stock is rated F/G (approximately 2% of those with mortgages), the challenges for these households appear particularly acute.

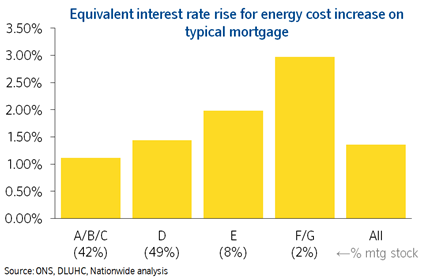

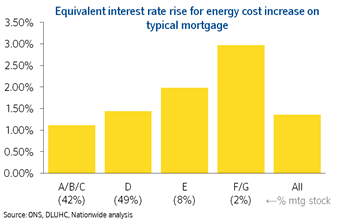

“To provide some further context of the scale of these increases, we’ve calculated the equivalent interest rate rise based on a typical outstanding mortgage. For ease of comparison, we’ve used the same mortgage balance and term for each EPC rating. Overall, the average increase is equivalent to a 1.36% rise in interest rates, but around 1% for A to C-rated properties, 2% for an E-rated property and nearly 3% for an F/G-rated property.

“Moreover, these increases in energy costs come at a time when mortgage interest rates are also rising. While most mortgages (c85%) are now on fixed rates, protecting borrowers in the short term, those who are looking to refinance face a significant rise in borrowing costs if mortgage rates stay at current levels. For example, the average rate on new two-year fixed rate mortgages is currently over two percentage points higher than those prevailing two years ago, while the average rate on five-year fixed rate mortgages is around 1.5 percentage points higher than five years ago.

“With household budgets coming under substantial pressure, the government is likely to increase support. But, as well as addressing the rising cost of energy bills, improving the energy efficiency of the housing stock could play a crucial role. Incentivising improvement measures, such as loft and cavity wall insulation and solar PV installations, could help limit bill increases and assist the UK towards its carbon emissions targets.”

-ends-