|

Headlines |

Jul-23 |

Jun-23 |

|

Monthly Index* |

516.6 |

517.8 |

|

Monthly Change* |

-0.2% |

0.1% |

|

Annual Change |

-3.8% |

-3.5% |

|

Average Price (not seasonally adjusted) |

£260,828 |

£262,239 |

* Seasonally adjusted figure (note that monthly % changes are revised when seasonal adjustment factors are re-estimated)

Commenting on the figures, Robert Gardner, Nationwide's Chief Economist, said:

“Annual house price growth edged down to -3.8% in July. This was the weakest outturn since July 2009, although it is only modestly lower than the -3.5% recorded last month. There was a slight fall of 0.2% over the month, after taking account of seasonal effects. As a result, the price of a typical home is now 4.5% below the August 2022 peak.

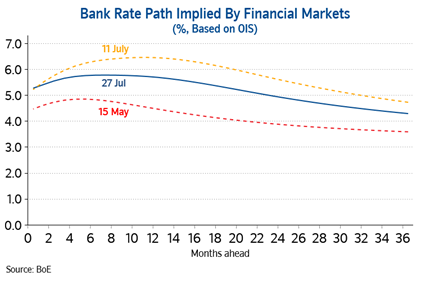

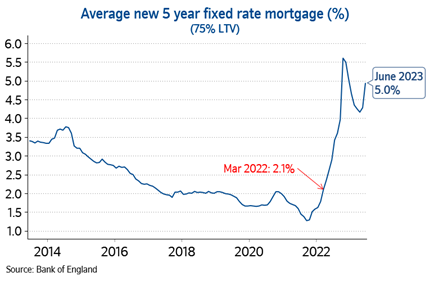

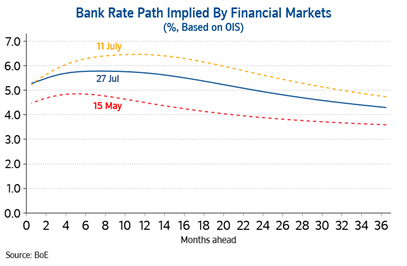

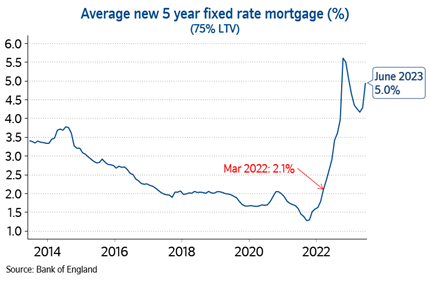

“Investors’ views about the likely path of UK interest rates have been volatile in recent months, with the projected Bank Rate peak fluctuating between 5% in mid-May and 6.5% in early July (see chart below). There has been a slight tempering of expectations in recent weeks but longer-term interest rates, which underpin mortgage pricing, remain elevated (see chart below).

“As a result, housing affordability remains stretched for those looking to buy a home with a mortgage. For example, a prospective buyer, earning the average wage and looking to buy the typical first-time buyer property with a 20% deposit, would see monthly mortgage payments account for 43% of their take home pay (assuming a 6% mortgage rate). This is up from 32% a year ago and well above the long-run average of 29%. Moreover, deposit requirements continue to present a high hurdle – with a 10% deposit equivalent to 55% of gross annual average income.

“This challenging affordability picture helps to explain why housing market activity has been subdued in recent months. There were 86,000 completed housing transactions in June, 15% below the levels prevailing the same time last year and around 10% below pre-pandemic levels. More timely mortgage approval data showed a slight increase in activity in June, though most of these applications will pre-date the more recent rise in longer term interest rates. Moreover, activity is still c20% below 2019 levels.

“Nevertheless, a relatively soft landing is still achievable, providing broader economic conditions evolve in line with our (and most other forecasters) expectations. In particular, unemployment is expected to remain low (below 5%), and the vast majority of existing borrowers should be able to weather the impact of higher borrowing costs, given the high proportion on fixed rates, and where affordability testing should ensure that those needing to refinance can afford the higher payments.

“While activity is likely to remain subdued in the near term, healthy rates of nominal income growth, together with modestly lower house prices, should help to improve housing affordability over time, especially if mortgage rates moderate once Bank Rate peaks.”

-ends-